9 Business Valuation Methods: What's Your Company's Value?

.png)

Whether you’re on the buy-side or sell-side, having an established accurate value of your business is an essential part of extracting value from a transaction. Those that are better able to value assets are the most successful investors of all time. And while you can add value to a transaction through a successful integration, paying the right price for a company gives you the best platform to do so.

In this article on business valuation, DealRoom borrows from some of the insights into valuation provided by colleagues that contributed to our sister site, M&A Science, as well as Founder & CEO at DealRoom and Chief Scientist at M&A Science, Kison Patel.

What is Business Valuation?

Company Valuation or Business Valuation, is the process by which the economic value of a business, whether a large or small business is calculated. The purpose of knowing the business’s value is to find the intrinsic value of the entire company - its value from an objective perspective. They are mostly used by investors, business owners and intermediaries such as investment bankers, who are seeking to accurately value the company’s equity for some form of investment.

Although business valuations are mostly used to value a company’s equity for some form of investment, this isn’t the only reason to have an understanding of a company’s value. A company is not unlike most other long-term assets, in that it’s useful to have a handle on how much it's worth.Being in an informed position at all times enables the company’s owners to understand what their options are, how to react in different business situations, and how their company’s valuation fits into the bigger picture.

The objectives for valuing a business can be divided into: internal motives, external motives, and mixed motives (being a combination of internal and external motives).

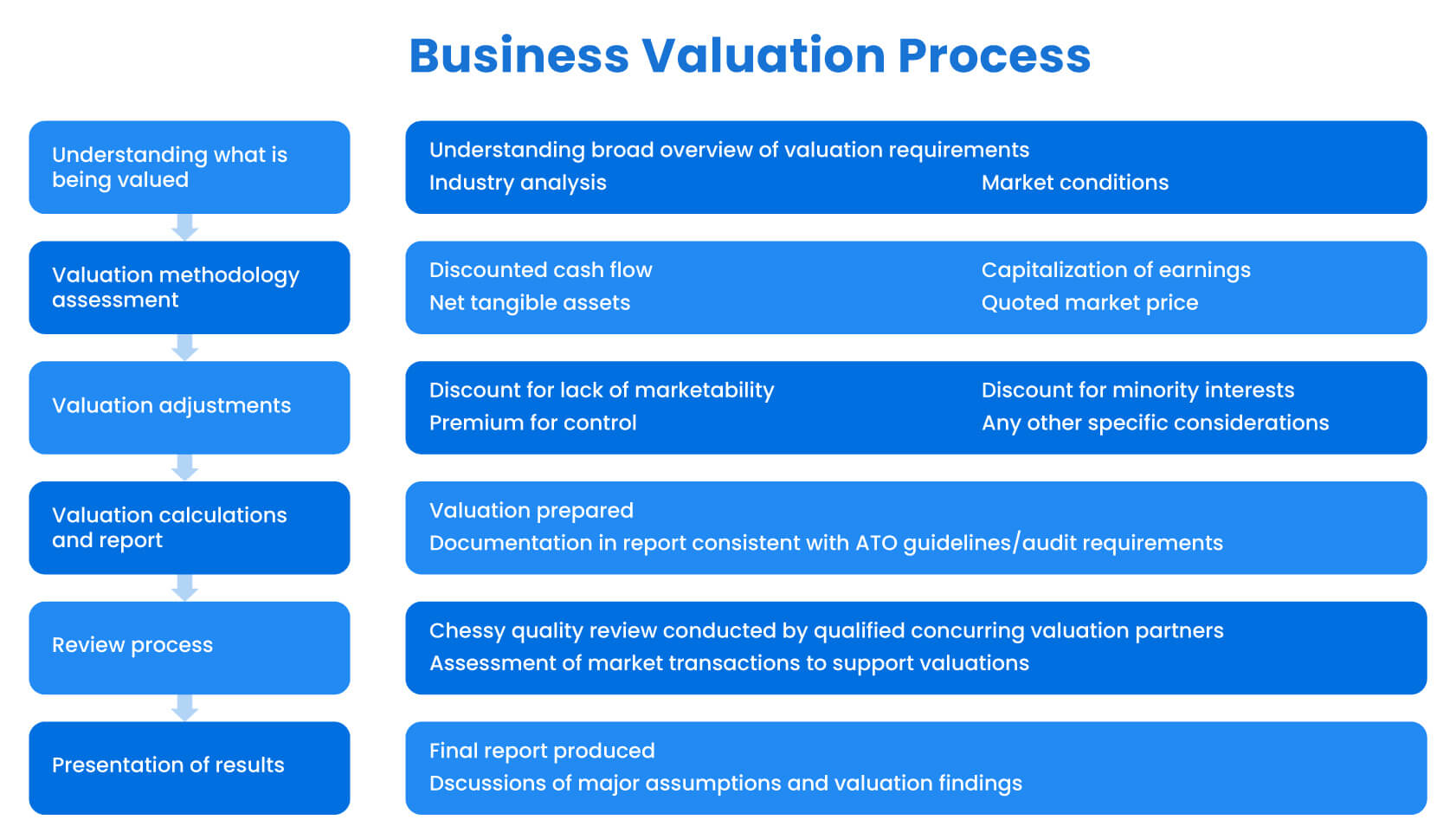

The Business Valuation Process

Every business valuation process differs based on which method you choose to evaluate.

Whatever the methods you use, the final aim is to find the company’s intrinsic value.

Depending on the company whether private companies or public companies, entrepreneurs or individuals conducting the business valuation process, the method can differ. For example, should a company be measured based on its assets, its future free cash flows, recent transactions for comparable companies, or the sum of its real options? More often than not, valuation professionals seek to use a combination of these to arrive at an answer.

The valuation methods they use are summarized in the table below

More often than not, business valuation professionals use at least two methods when valuing companies, the most common being the DCF method and comparable transactions.These methods are popular because they’re widely understood, but also because the underlying numbers are easier to obtain. In the case of real options valuation, for example, the numbers which underpin the value of the business are far more difficult to objectively ascertain.

Business Valuation Methods

- Discounted Cash Flow Analysis

- Capitalization of Earnings Method

- EBITDA Multiple

- Revenue Multiple

- Precedent Transactions

- Liquidation Value / Book Value

- Real Option Analysis

- Enterprise Value

- Present Value of a Growing Perpetuity

1. Discounted Cash Flow Analysis

Discounted cash flow analysis uses the inflation-adjusted future cash flows to project a value for the business.The thinking behind DCF Analysis is that free cash flows are what endow shareholders with value and only that number that matters.

The problem then arises of how to accurately project discounted free cash flows (FCF), using a weighted average cost of capital (WACC) several years into the future. Even small differences in the metrics, growth rate, the perpetual growth rate and the cost of capital can lead to significant differences in valuation, fueling criticism of the method.

DCF = CF1 / (1+r)1 + CF2 / (1+r)2 + ....+ CFn / (1+r)n

Where, CF1 = The cash flow for year one, CF2 = The cash flow for year two, n = Number of years, r = Discount rate

For example, let's consider a company with projected FCF of $1 million for the next 5 years. Assuming a discount rate of 10%, the company's future cash flows amount to approximately $3.79 million.

2. Capitalization of Earnings Method

The capitalization of earnings method is a neat, back-of-the-envelope method for calculating the value of a business, which in fact is used by DCF Analysis to calculate the perpetual earnings (i.e. all those earrings that occur after the terminal year of the DCF Analysis being performed).

Sometimes called the Gordon Growth Model, this method requires that the business have a steady level of growth and cost of capital.The numerator, usually the free cash flow, is then divided by the difference between the discount rate and the growth rate, expressed as fractions to arrive at an approximation of a valuation.

Market Capitalization = CF1 / (r-g)

Where, CF1 = Cash flow in the terminal year, r = Discount rate , g = Growth rate

For example, consider a company with projected FCF of $1 million in the terminal year, a discount rate of 10%, and a growth rate of 5%. Using the capitalization of earnings method, the value of the company would be approximately $20 million.

3. EBITDA Multiple

The EBITDA multiplier is an excellent solution to the arbitrary nature of most valuation methods. Even Aswath Damodaran, the father of modern valuation, says that any valuation of a business should follow the law of parsimony: the most simple of two (or more) competing theories should hold sway in an argument.

On this basis, the EBITDA multiple - the multiplication of this year’s EBITDA figure by a multiplier agreeable to both the buyer and seller - is an elegant solution to the valuation dilemma.

Even those who consider this method too simplistic tend to use it as a guide for their valuations, underlining its strength.

4. Revenue Multiple

This method can be used in those circumstances where EBITDA is either negative or isn’t available for some reason (usually because sales figures are the only ones available when researching firms to acquire through online search).

Again, while you might say it’s just a benchmark - others would argue, with some justification, that the total sales of a business is the most important benchmark of all.

5. Precedent Transactions

This method may incorporate the EBITA and revenue multipliers or any other multiple that the practitioner wishes to use. As the title suggests, here the valuation is derived from comparable transactions in the industry.

So, for example, if widget makers have been trading at multiples of somewhere between 5 and 6 times EBITDA (or net income, or whatever indicator is chosen), Widget Co. would establish its value by performing the same iterative process.

The problem that then arises, is how similar are companies to others, even in their own industry?

Thus, for our money, this is more of a barometer of the market than a valuation method per se.

6. Book Value/Liquidation Value

The liquidation value is what Warren Buffett claims to have always looked at when seeing if businesses are overvalued on the stock market or not.This value is the net cash that a business would generate if all of its liabilities were paid off and its assets were liquidated today.

In a sense, calling this a valuation method for a business is a misnomer - this only gives you the value of part of the business.

But, to paraphrase Buffett, it allows you to see the ‘margin of error’ that you have with a valuation.

The logic goes that, even if everything goes wrong in management and the company’s sales fall dramatically after the acquisition, it can always fall back on the liquidation value.

7. Real Option Analysis

Proponents of real options analysis look at businesses as nothing more than a nexus of real options: the option to invest in opportunities, the option to utilize spare capacity, the option to hire more salespeople, etc.

Bringing together these options is the basis behind real options analysis for valuation.

This is most effective for firms with uncertain futures, usually those who aren’t yet cash generative: startups and mineral exploration firms, for example.

Of the valuation methods on this list, it’s by some distance the most complicated but its proponents include McKinsey and several of the world’s most prestigious business schools.

8. Enterprise Value

Enterprise Value (EV) is a method to measure the company’s total market value where we not only consider the company's equity but also its debt obligations and cash reserves.By including debt, we can provide a more accurate picture of a company’s value, especially in the context of mergers or acquisitions, as it represents the total cost to acquire the company’s operations.

EV = Market Capitalization + Total Debt - Cash and Cash Equivalents

For example, if a company has a market capitalization of $50 million, total debt of $20 million, and cash reserves of $5 million, its enterprise value would be $65 million ($50M + $20M - $5M).

9. Present Value of a Growing Perpetuity

The Present Value (PV) of a Growing Perpetuity is a valuation method which is used to estimate the total value of cash flows that continue indefinitely and grow at a constant rate. It's often applied in situations where cash flows are expected to continue indefinitely, such as in perpetuity. We can calculate the present value of a growing perpetuity with:

PV = C / (r-g)

Where, C = Cash flow at the end of the first period. r = Discount rate, g = Growth rate

For example, if a company generates a cash flow of $1 million at the end of the first period, and the discount rate is 8%, with a growth rate of 3%. Then the present value of the growing perpetuity would be $20 million.

How to Pick the Right Valuation Method?

The last section mentioned how most business valuation professionals use at least two methods of valuation, and also that the valuation (the output) will ultimately only be as good as the numbers used to achieve it (the inputs).

After conducting a preliminary analysis of the company, whoever is conducting the valuation chooses the method, which is most suitable to the business and its industry.

There is no question that the biggest determinant of the valuation method used is available information. To take the example of comparable transactions, without any reasonably comparable transactions, there is no way that this valuation method can be conducted.

Here is an example of intangible assets valuation.

Even transactions in the same space from several years before cannot be considered accurate representations of a company’s value in the current environment.

In a similar vein, even the most commonly used valuation method, the DCF method, requires users to forecast free cash flows to a predetermined point in the future. Only in the most extreme cases - for example, a company with a remarkably small number of clients and pre-agreed contracts - is this feasible.

But information is just one of the factors which should determine which is the right valuation method to choose. The others are as follows:

Type of the company

If a company is asset-light, such as is the case with many service companies, it makes little sense to use the net-asset valuation method. Similarly, if most of a company’s value is in its branding or IP, it may make little sense to use the discounted cash flow method.

Size of the company

Larger companies tend to be applicable for a larger number of valuation methods. Small companies, with less information, are usually only subject to a handful of valuation methods. Bear in mind too that different valuation considerations are at play for each (e.g., higher valuation multiples for larger companies).

Economic environment

Regardless of which method is chosen, it’s never a bad idea to consider the economic environment that the company faces. But in more positive economic conditions, it’s important to be somewhat conservative when valuing in the understanding that all business cycles come to an end.

End users

A further consideration for valuing a company is what the end user requires the valuation for. Some buyers will only look at the value of a company’s fixed asset value, be that technology, real estate, or even trucking. Others will only be interested in cash-flow generating potential (as is the case with most buyers of SAAS platforms).

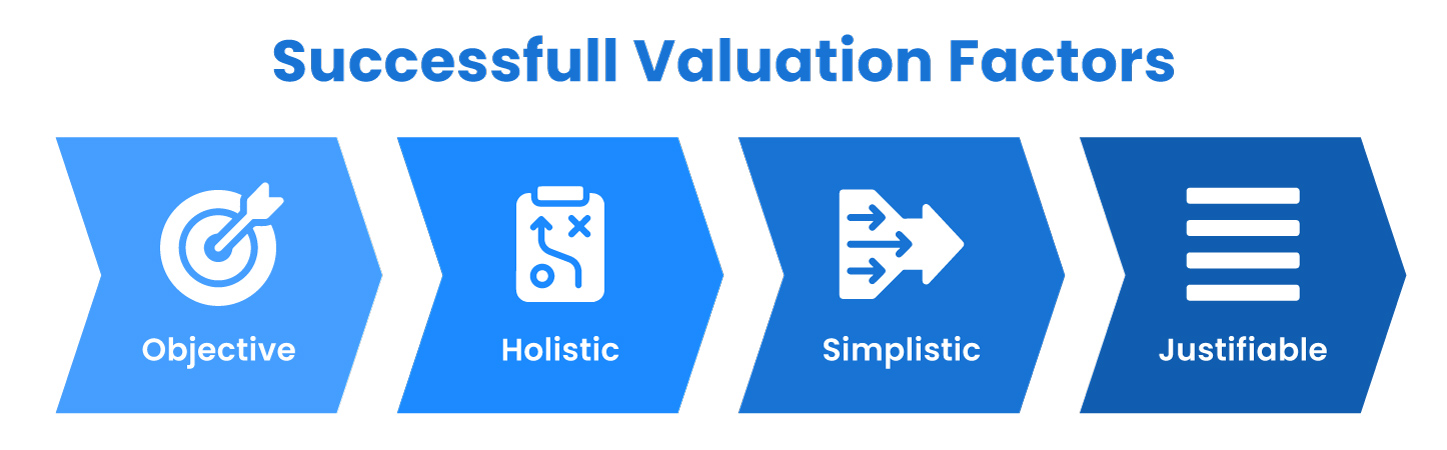

How to carry out a successful valuation of a company

There are a few ways in which a valuation professional can ensure that, whatever the valuation method they choose, they’ll arrive at a number which approximates intrinsic value.

Successful valuation factors are:

Objective

A valuation which is heavily influenced by an opinion can be regarded as just that - an opinion.

Holistic

The valuation should consider as much as possible; not just a company’s assets or its cash flows, but also its environment, and other internal and external factors.

Simplistic

Holistic does not mean detail for the sake of detail. Valuing Amazon doesn’t require making projections about the future prices of cardboard packaging.

Justifiable

Anyone reading the valuation should be able to arrive at the same conclusion as the individual conducting the valuation based on the information provided.

Business valuation providers

Business valuation is the bread and butter of investment banks and M&A intermediaries.

Even if a company has the wherewithal to conduct their own business valuation, it pays to hire a third party specialist for the expertise that they bring to the task. Even legal firms now typically have an in-house valuations expert.

Depending on the valuation method(s) used by the business valuation providers, the company can change the inputs over time to see how their valuation evolves.Accredited business valuation providers can also ensure reliable and accurate valuations. These specialists adhere to industry standards and bring valuable insights to the table, enabling companies to make informed decisions regarding their valuation strategies.

Closing Remarks

The minute-by-minute fluctuation of the stock prices reflect the reality that there can never be a true consensus on a company’s valuation: Everybody has their own.

Blue chip Investment banks, keen to let everybody know that they’re hiring the best quantitative analysts in the world, can also vary widely on price. The upcoming IPO of British chip manufacturer ARM is a case in point. The value of the IPO pitched by investment banks has ranged from $30 billion to $70 billion - a massive $40 billion difference. Most of these bankers will be wrong by billions of dollars, illustrating the difficulty of business valuations.

What links all of the methods mentioned here is that their users have, at one time or another, plugged numbers into a model which gave a number they thought was erroneous, only to replace the numbers moments later to arrive at a number they considered ‘more reasonable’. The best advice is to use as many measures as possible to arrive at a valuation. The more insights you can garner on its revenues, EBITDA, free cash flows, assets and real options, the better a perspective you gain of the company’s true value.

The DealRoom M&A Optimization Platform optimizes the M&A process and makes it more efficient.Whether you need an advanced M&A pipeline tool to enable pipeline management and reporting or a data room software to manage all your diligence requests, DealRoom has the solution for you.

%20(1).jpg)

.jpg)

.jpg)

.jpg)

Get your M&A process in order. Use DealRoom as a single source of truth and align your team.

.svg)

.png)